Area median income: What it means and how it’s calculated

Photo via Flickr cc

If you’ve ever applied for affordable housing in New York City, you’ll know that it is all about the area median income, or the AMI. If you make too little or too much, you won’t qualify at all for affordable housing. Even if you do qualify, however, your AMI will impact your likelihood of actually acquiring a unit since most buildings have more units available in some AMI bands than others. For most New Yorkers, this is one of the most confusing aspects of affordable housing, so we’ve broken it down, from how AMI is calculated and what the current NYC parameters are to the many controversies surrounding the guidelines.

How the AMI is calculated

The AMI is an income figure used to help determine eligibility for affordable housing programs in New York City and is calculated on an annual basis by the U.S. Department of Housing and Urban Development (HUD). HUD calculates a median family income for each metropolitan area and each nonmetropolitan county in the United States using data from the American Community Survey. If no data is available for a specific year, HUD uses the most recent data but accounts for inflation by taking the actual and forecasted Consumer Price Index into account.

The current AMI in New York City

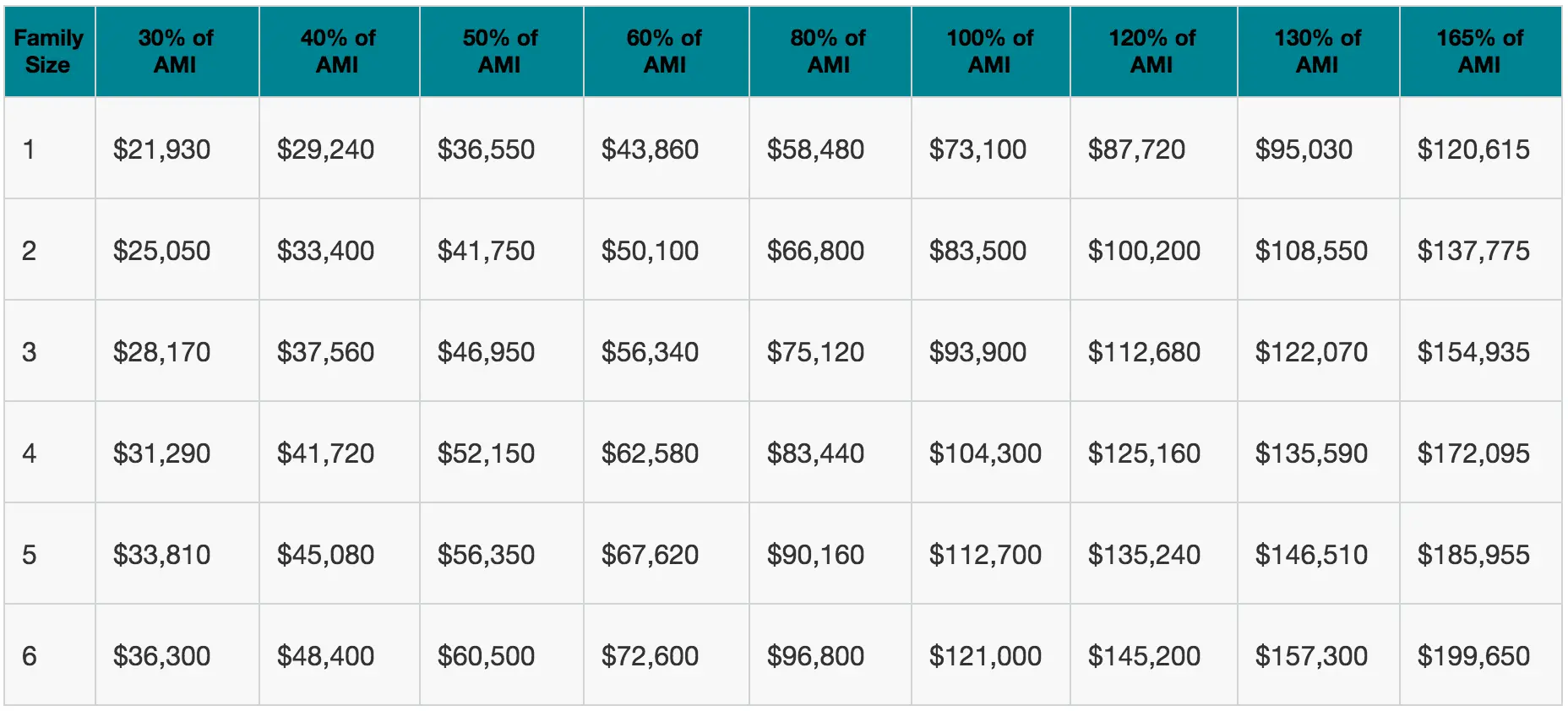

The AMI is first and foremost used as a guide to determine who is and is not eligible for different types of housing programs. Below are New York City’s 2018 levels; the 2019 AMI will be released later this year.

Chart created by 6sqft

Chart created by 6sqft

What the AMI effects

The AMI primarily impacts who is eligible for affordable housing. While many people assume that affordable housing only impacts people living on low incomes, in fact, it affects people living on both low and middle incomes. Sometimes another term—the area’s median family income (MFI)—is used interchangeably with AMI. MFI, not AMI, is generally the term used in relation to housing programs targeting very low-income families, including the Section 8 voucher program.

Controversy over the AMI in New York City

One of the most controversial aspects of the AMI is that it is calculated by HUD and not the City of New York. As a result, New York City’s AMI actually includes several affluent suburbs, including Westchester, Rockland, and Putnam counties. Given that all three suburbs are generally assumed to have higher area median incomes than New York’s five boroughs, many people also assume their inclusion artificially inflates the AMI in New York City. In August 2018, for example, City & State ran an article on this issue observing, “New York City’s AMI is inflated by the inclusion of income data from affluent suburbs, meaning what the city may designate as affordable housing may not be affordable for many city residents – and especially not for the residents of the neighborhood itself.”

While many New Yorkers argue that local AMI is being artificially inflated by HUD due to the inclusion of several nearby suburbs, an article published by the NYU Furman Center in late 2018 suggests that this is a misconception: “Because HUD uses Westchester, Rockland, and Putnam counties in its calculation of NYC’s AMI, many assume that these counties’ more affluent areas are pulling affordable housing beyond the reach of the neediest households in the five boroughs. But removing Westchester, Putnam, and Rockland Counties from HUD’s AMI calculation would not significantly change the metro-wide result.”

Still, many people continue to question the wisdom of basing affordable housing eligible on the AMI. After all, should a family earning more than $100,000 per year be eligible for affordable housing when the city is currently struggling to house families with no stable housing at all, including an estimated 15,485 homeless families with 22,899 homeless children? Again, while it is easy to blame the AMI alone, researchers at the Furman Center note that the AMI is not really to blame. After all, local policymakers can lower the income levels subsidized housing will serve—for example, they can choose to target households at 30 or 50 percent of the AMI as opposed to 60 percent. The real problem, then, may not be the AMI but rather how local authorities choose to use it to set guidelines for affordable housing.

RELATED:

Get Insider Updates with Our Newsletter!

Leave a reply

Your email address will not be published.

Your blog post was well-structured and easy to understand. I appreciated the practical examples and the actionable advice you shared. To gain more knowledge, click here.

so how do the cal rent on inco me 0f 60% ami